The world's problem is ours too.

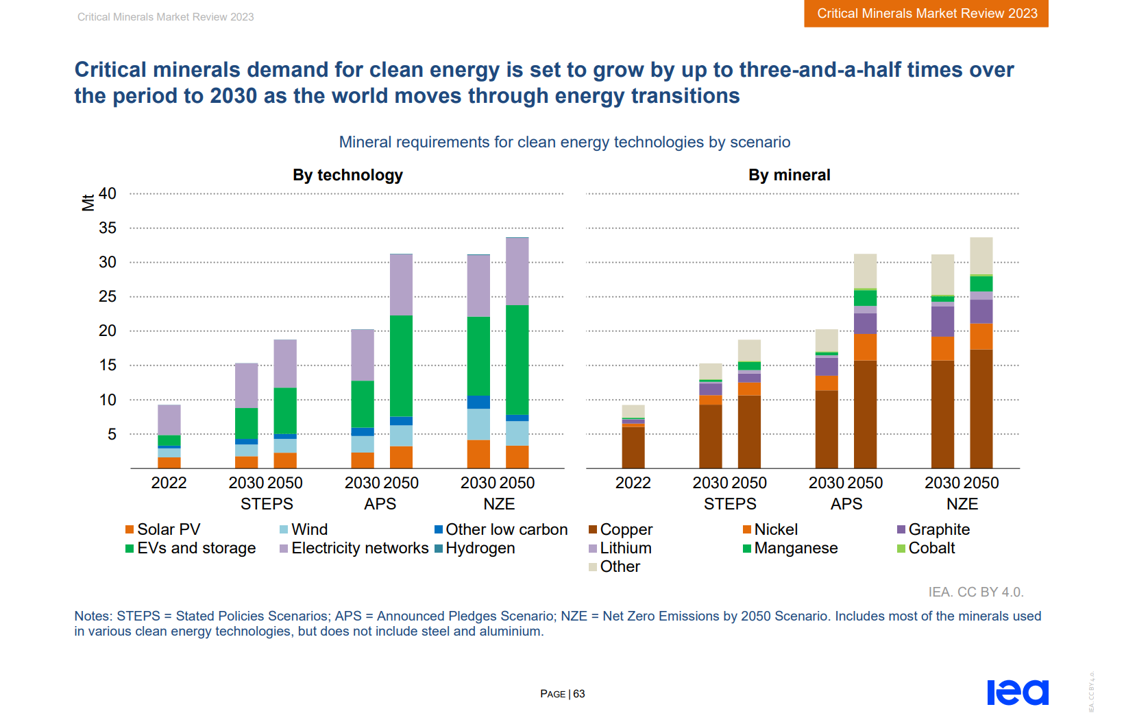

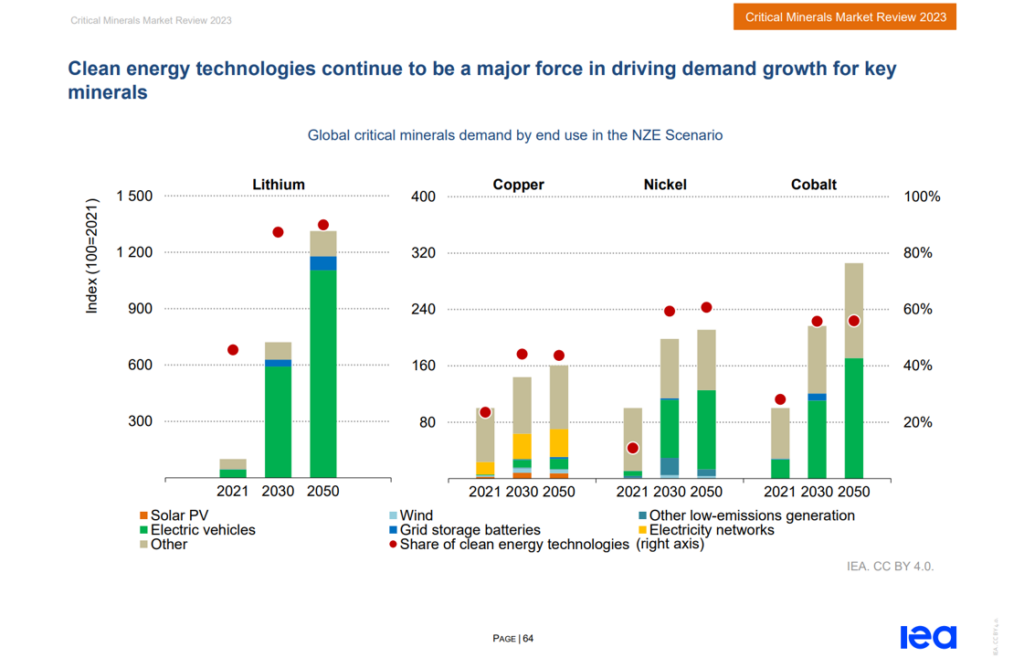

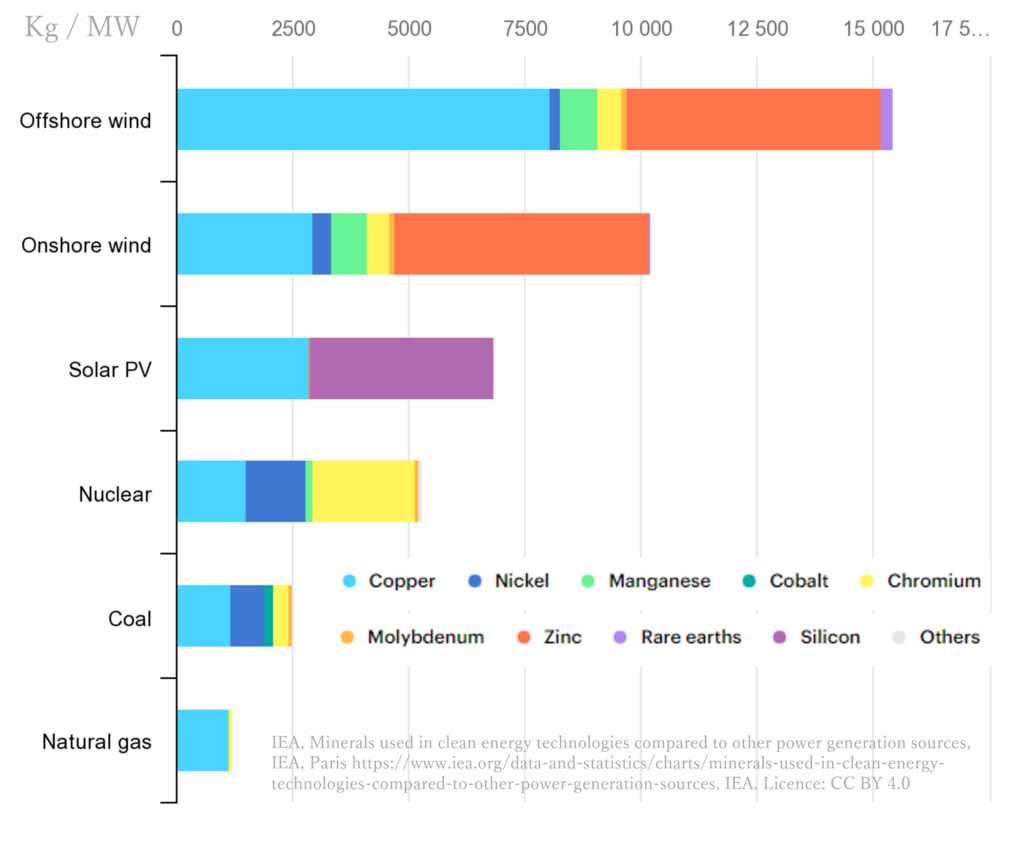

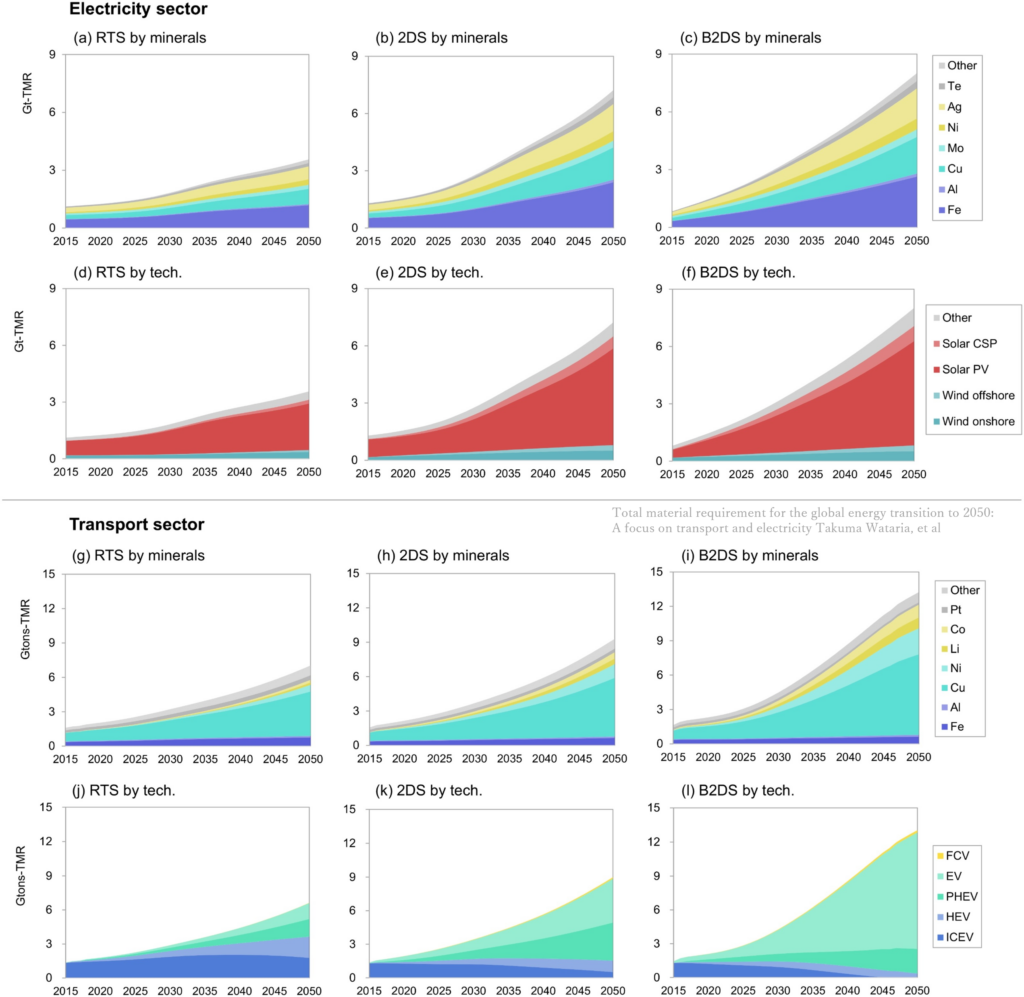

Critical minerals are a fundamental part of the energy and electricity security landscape. Demand for critical minerals for clean energy technologies is set to rise two to fourfold by 2030 (depending on the scenario) as a result of the expanding deployment of renewables. Copper use sees the largest increase in terms of absolute volumes, with current demand of around 6 million tonnes (Mt) per year increasing to 16 Mt in the NZE Scenario.

International Energy Agency | World Energy Outlook 2022 EVs, battery storage and electricity networks.

• Stated Policies Scenario (STEPS): this scenario maps out a trajectory that reflects current policy settings, based on a detailed assessment of what policies are actually in place or are under development by governments around the world.

• Announced Pledges Scenario (APS): this scenario assumes that all long-term emissions and energy access targets, including net zero commitments, will be met on time and in full, even where policies are not yet in place to deliver them.

• Net Zero Emissions by 2050 (NZE) Scenario: this scenario sets out a pathway for the global energy sector to achieve net zero CO2 emissions by 2050.

As the world moves on from today’s energy crisis, it needs to avoid new vulnerabilities arising from high and volatile critical mineral prices or highly concentrated clean energy supply chains. If not adequately addressed, these issues could delay energy transitions or make them more costly.

In the Announced Pledges Scenario (APS), demand for critical minerals more than doubles from today’s level by 2030. In absolute tonnage, Copper sees the largest increase but other critical minerals experience much faster rates of demand growth, notably silicon and silver for solar PV, rare earth elements for wind turbine motors and lithium for batteries. Demand management through sobriety, innovation in technologies with low metallic intensities, and efficiency gains -within the limits of the laws of physics- continued recycling in mature sectors are vital options to ease strains on critical minerals markets.

Both the extraction and processing of critical minerals are highly concentrated geographically: unless the need for stronger resilience and diversity in supply chains is addressed, there is a risk that the increasing use and importance of critical minerals could become a bottleneck for clean energy deployment. High reliance on individual countries such as China for critical mineral supplies and for many clean technology supply chains is a risk for transitions, but so too are diversification options that close off the benefits of trade.

Endgame of Easter Eggs chase ?

Transitioning « away » from fossil fuels is definitely not enough to stay on a 1.5 degrees pathway , and we all know it. Neither is « phasing down » actually. Futureproofing businesses means seriously considering the risk of an era with little to no access to fossil hydrocarbons. If not restricted from a self-imposed diet on black gold, an interrupted supply from increased geopolitical tensions, energy return on energy invested too poor for operators to keep going, yielding prohibitive marginal cost of production, or utmost depletion of the finite quantity of oil available, having reached planetary boundaries. Rather than forced sobriety, planned reduction and decreased reliance may be the way…

Coal, Oil and Gas are not the only commodities seeing increase in the discovery cost, and higher energy requirements.

As most of the easy-to-find deposits have been discovered, metal explorers are facing the dilemma of looking for high-grade orebodies under difficult conditions (deep underground buried below thick cover) or lower grade surface deposits or tailings reprocessing of potentially challenging metallurgically. With ever lowering grades, the waste-to-ore ratio increase, symmetrically increasing the energy requirement .

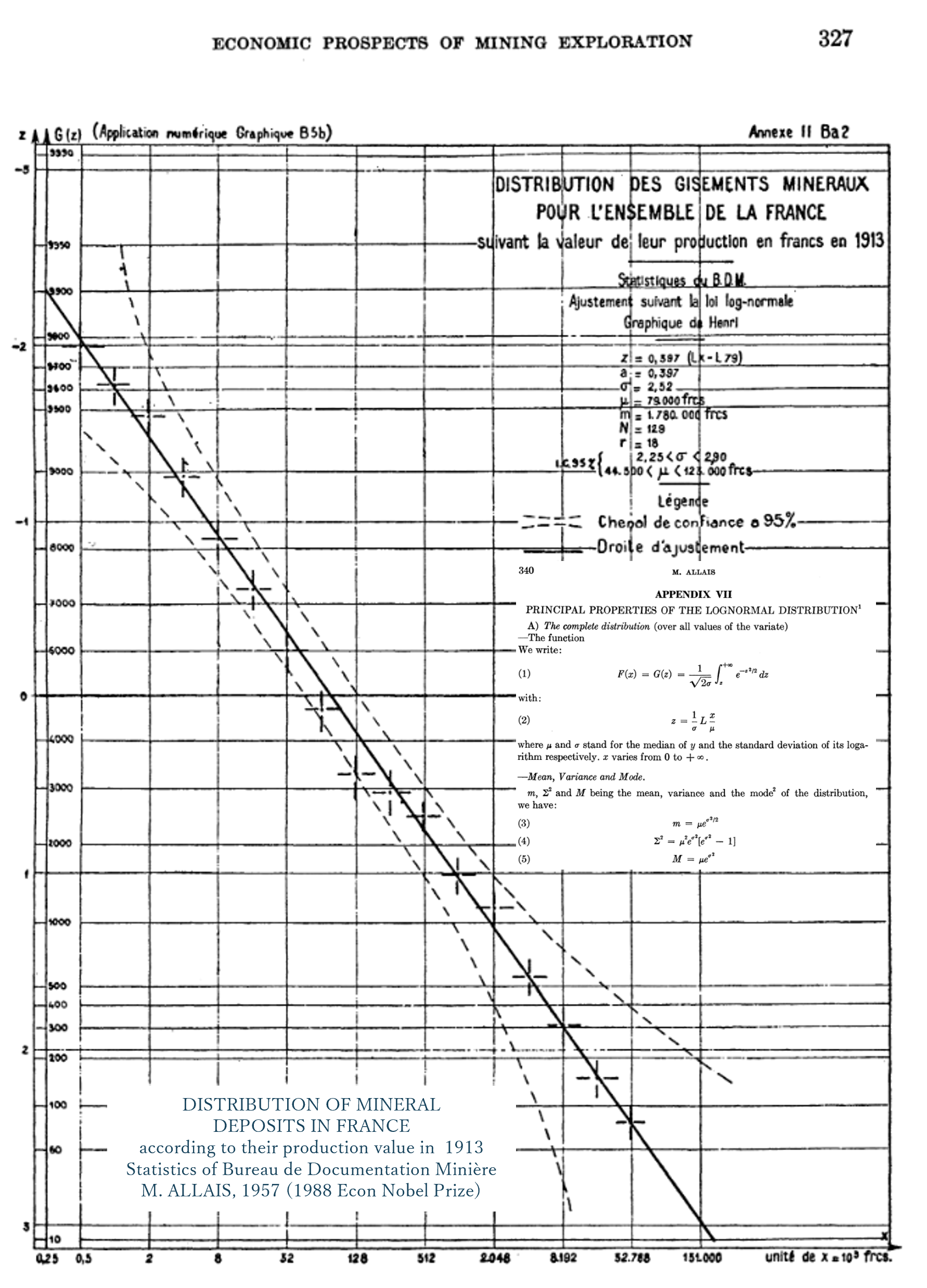

The lognormal distribution of metals grades, and its consequences to us

As grades can’t be be negative, zero acts like a hard boundary.

Given this remains true across all commodities, the odds of finding the top 1% mineral endowment decreases exponentially.

An efficient utilisation of resources calls for the highest grades to be targeted, found and mined first, easier said than done.

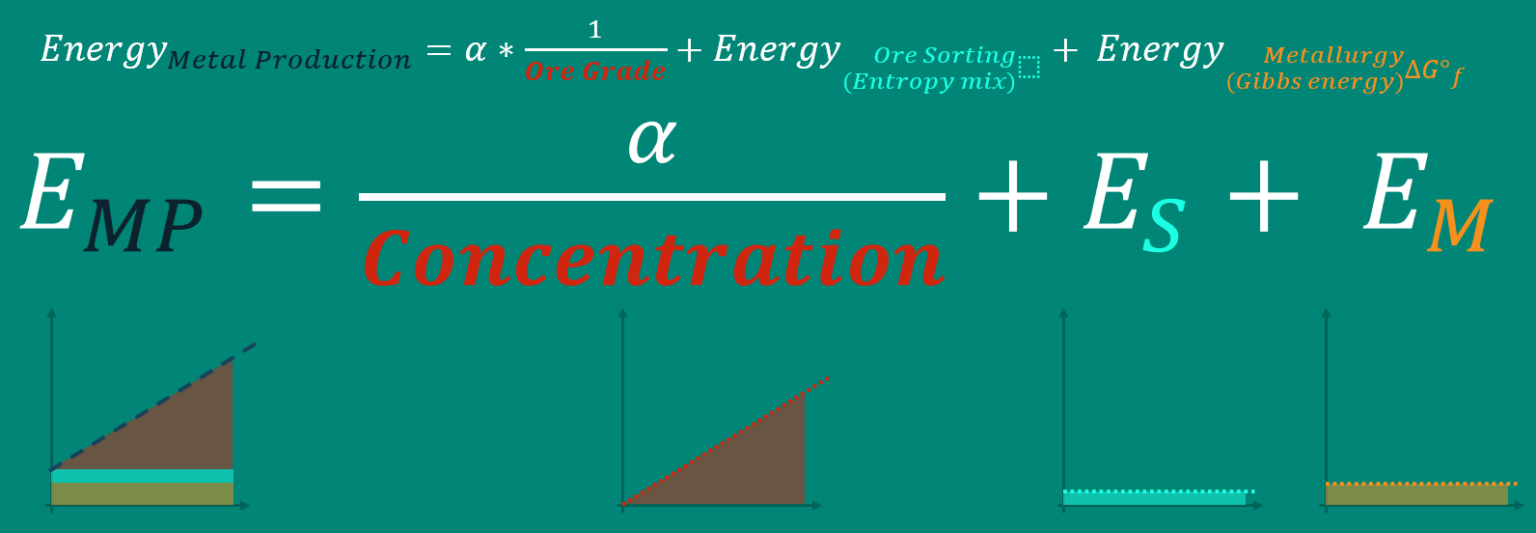

Beyond grades : the energy for metal production

The first term of the energy requirement is a function of the inverse of the concentration, said otherwise, it’s proportional to 1 over the grade.

That is, the lower the metallic concentration in the ore, the more mass needs be mined, and subsequently crushed. The other terms are constants. Overall, the energy required for the metal production is increasing overtime, as we mine lower grade deposits.

The energies of copper production

CU later, Copper !

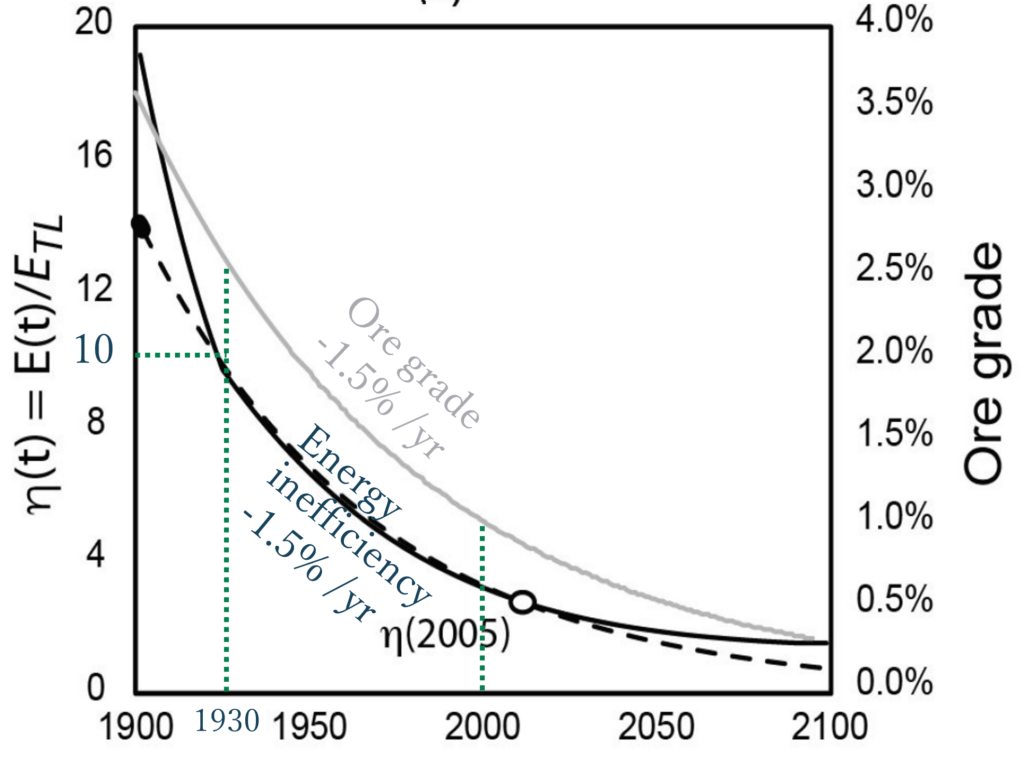

The price of copper from 1900 to 2000 has dropped by 1-2% per year essentially dominated by increased energy efficiency.

Until the 2000s, the energy gains compensated the decreasing cut-off concentrations.

Efficiency gain 1930 – 2000 : -1.5% / year

Ore grade 1930 – 2000 : -1.5% / year

-1.5% / year won’t last forever.

The thermodynamic limit η=1.5 will be reached before 2100.

Improvement in mechanical crushing and grinding technologies won’t be able to happen as quickly as the drop in concentration of ore reserves.

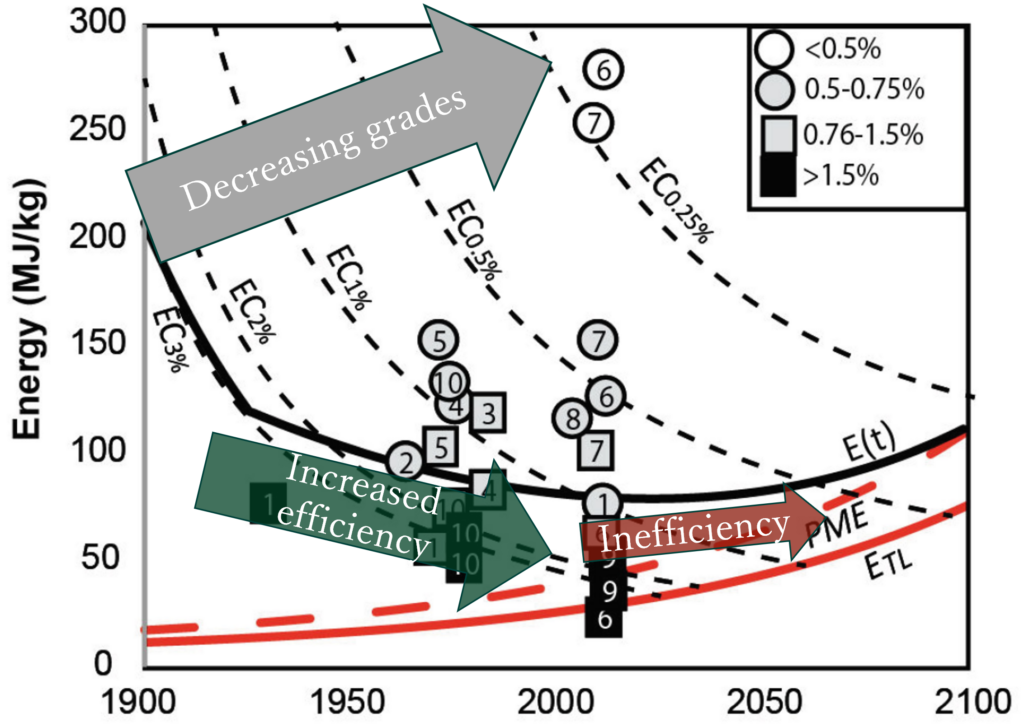

The limit of efficiency gains

The ever-increasing energy requirement of lower grade ore is the thermodynamic baseline (in red). Yet, as there is no such things as 100% efficiency, a more realistic dotted line highlights the practical minimum energy expected to be required for the production of copper, as the 3% deposits are getting exhausted, replaced with 2%, then 1% and even massive low-grade Andean porphyry in the 0.5% copper mark.

Hitting the baseline

While there has been significant increase in efficiency in the past century, it’s essentially because there was much room for improvement. (the distance to the thermodynamic limit is decreasing in a 1⁄e^x fashion).

Now we are getting very close the best that can be done, and it is expected that the rest of the century will see an increase in the energy requirements, driven by the forever decreasing drop in concentration of orebodies.

- Energy of copper production with varying ore grade and technology E(t)

- Energy at constant ore grade with varying technology (EC)

- Practical minimum energy (PME)

- Thermodynamic limit (ETL)

With the grades of new deposits falling, the overall endowment of reserves is increased. But let’s not be fooled by seemingly unlimited tonnages of ore available at lower grades, as the mobilisation of resources required to convert it in usable metal is increasing simultaneously. As concentrations are still 200 times richer than the average content of copper in the crust (Clark Cu = 30 ppm = 0.003%)

Vidal, O.; Le Boulzec, H.; Andrieu, B.; Verzier, F. Modelling the Demand and Access of Mineral Resources in a Changing World. Sustainability 2022

Rötzer and Schmidt [89]; (2) Rosenkranz [90]; (3) Gaines [91]; (4) Kellogg [92]; (5) Page and Creasy [93]; (6) Norgate and Jahanshahi [86]; (7) Marsden [94]; (8) Office of Energy Efficiency and Renewable Energy [95]; (9) Rankin [96]; (10) Chapman [97]

What comes down must go up

Can prices go any lower ?

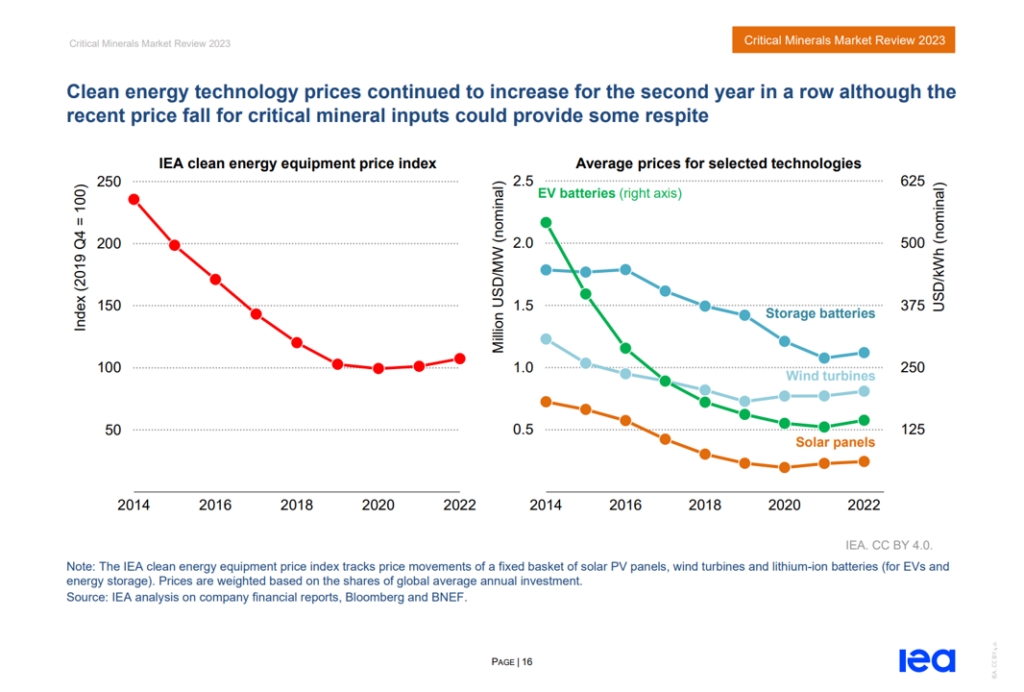

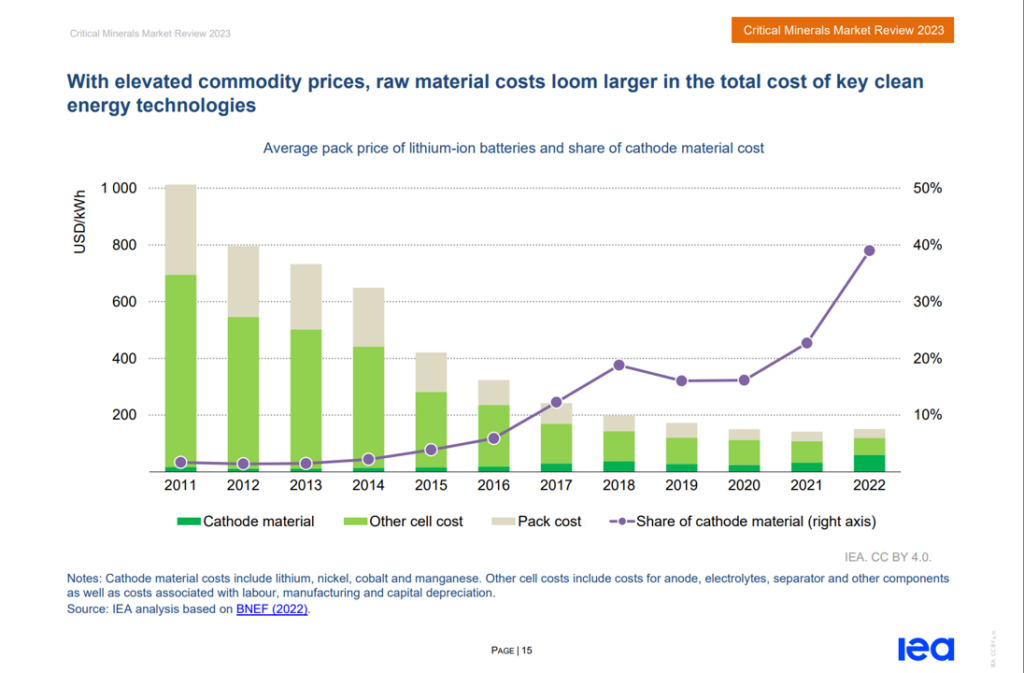

Metal-intensive low-carbon technologies costs have consistently decreased until around 2020, when the curves flattened. While efficiency gains have helped make these techs more affordable, durable increase in energy priced have steadily been counteracting any financial savings.

No one can escape the laws of physics, not even solar panel manufacturers. The thermodynamic maximal yield of current cells is nearly reached. Remaining improvement through economies of scales have been achieved in gigafactories, leaving a thin margin for extra progress to be expected, and the $/kWh is forecasted to increase. A fossil-fueled world made these technologies cheap, the maximal affordability is now behind us, and low-cost renewable generation will go away as upstream fossil-reliant manufacturing and shipping processes have to cope with their geologically-imposed phase out, and costlier alternative. As a result, now is the best time in history to invest in inexpensive electrification.

Our appetite for critical minerals

Not all metals are created equals

At Akarbo, we believe that some elements are more worth chasing than others. While not all the information can be contained in a price, it appears that the industry discriminate against the different commodities too, judging but market size.

We like Copper because of the sheer volumes of this essential red conductor required. So much so that it deserved it’s own axis, otherwise it would dwarf the other metals.

As long as the mineral has a critical role for the energy transition, we are metal-agnostic. We target altogether IOCG-IOA for their Cu,Co,REE,U content, Carbonatites for their REE grades, and LCT pegmatites (Li,Si) indifferently.

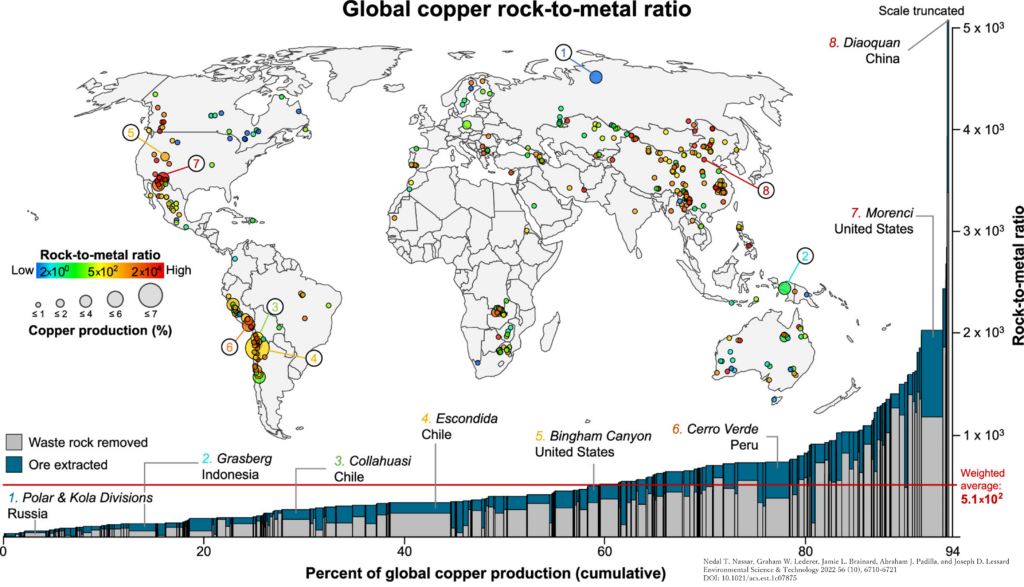

Optimising the rock to metal ratio

We want to be leaders in metal to waste ratio, both by targeting world class, high grade deposits, and developping integrated business where waste doesn’t have to be, and is just another resource looking for a market.

We won't explore for gold, nor diamonds.

Without surprise

Aspiring to best-in-class grades

Optimising the rock to metal ratio

We want to be leaders in metal to waste ratio, both by targeting world class, high grade deposits, and developping integrated business where waste doesn’t have to be, and is just another resource looking for a market.

WA, critical mineral powerhouse

Integration of isotopic and seismic data

New insights from geochemical and isotopic mapping, seismic surveys, to reference this back to poorly mapped undercover geology, to increase our applied understanding of cratons, the evolution of their margins, and the associated deposits their bear.

Integration of DMIRS & GSWA work should help reveal the internal architecture, through various techniques covering data of varying amplitude, from crustal scale seismic reflection surveys, to passive seismic arrays, to regional isotopic maps, or whole rock geochemistry from publicly funded EIS drillholes.

Depletion of a finite endowment

Unlocking "The Gap"

Proterozoic margins have more to give

We want to be leaders in metal to waste ratio, both by targeting world class, high grade deposits, and developing integrated business where waste doesn’t have to be, and is just another resource looking for a market.

Integration of isotopic and seismic data

New insights from geochemical and isotopic mapping, seismic surveys, to reference this back to poorly mapped undercover geology, to increase our applied understanding of cratons, the evolution of their margins, and the associated deposits their bear.

Integration of DMIRS & GSWA work should help reveal the internal architecture, through various techniques covering data of varying amplitude, from crustal scale seismic reflection surveys, to passive seismic arrays, to regional isotopic maps, or whole rock geochemistry from publicly funded EIS drillholes.

The reason we won't ever explore for gold

The yellow metal abundance in the crust (0.001-0.006 parts per million), requires a thousand fold enrichment through geological processes, to achieve grades around 1 ppm to qualify for reasonable prospect of economic extraction.

With an average Rock-to-metal Ratio of 5 million (0.5 gram of gold metal recovered per ton) of ore, not considering for the stripping (or ore-to-waste ratio), this makes it amongst the most diluted commodity, and thus the most energy & CO2e intensive activity.

Just because we can, doesn't mean we should

Many explorers raise funding to prospect for gold. Some find anomalies worthy of additional consideration, and some few may even become a short-lived mine. And 2.5% of the profit goes back to the state as royalty ! What a generous contribution to society !

An alternate future could have happened, one where the explorer’s :

- hours of brain juice,

- workforce’s shifts,

- use of physical goods,

- mobilisation of (mostly) fossil energy and drilling machinery

would have ended up with the discovery of a deposit of a metal actually useful for the energy transition !

The real world is constrained with finite resources – human or material – and the question of their optimal allocation will always arise, all together with ultimate looming opportunity cost.

Exploring with purpose would have equally yielded :

- Intellectual stimulation of exploration geos,

- upskilling of field team through additional experiences,

- purchase of goods with GST and local expenditure,

- Use of energy and equipment contractors

would have happened regardless, but in the later case, a metal that matter (pick one, there are a few in the periodic table, just not #79)

Despite all of this effort, energy spent in developing that prospect,

Self-imposed values, or the power to say no

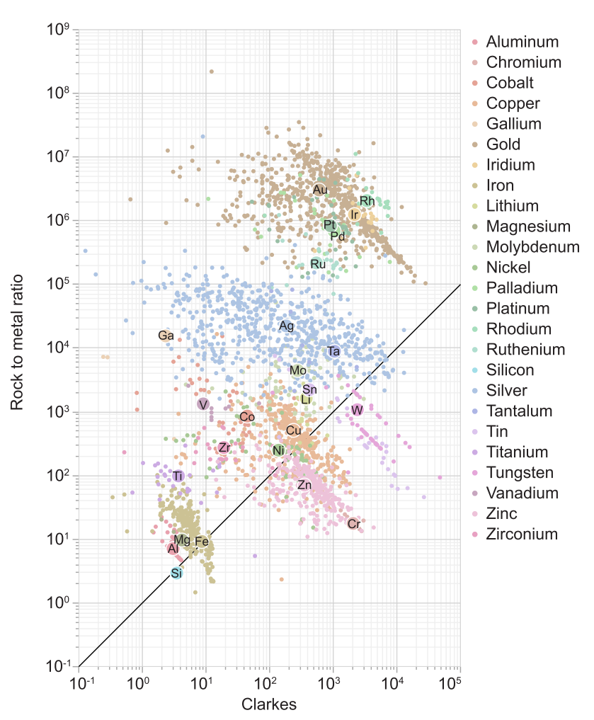

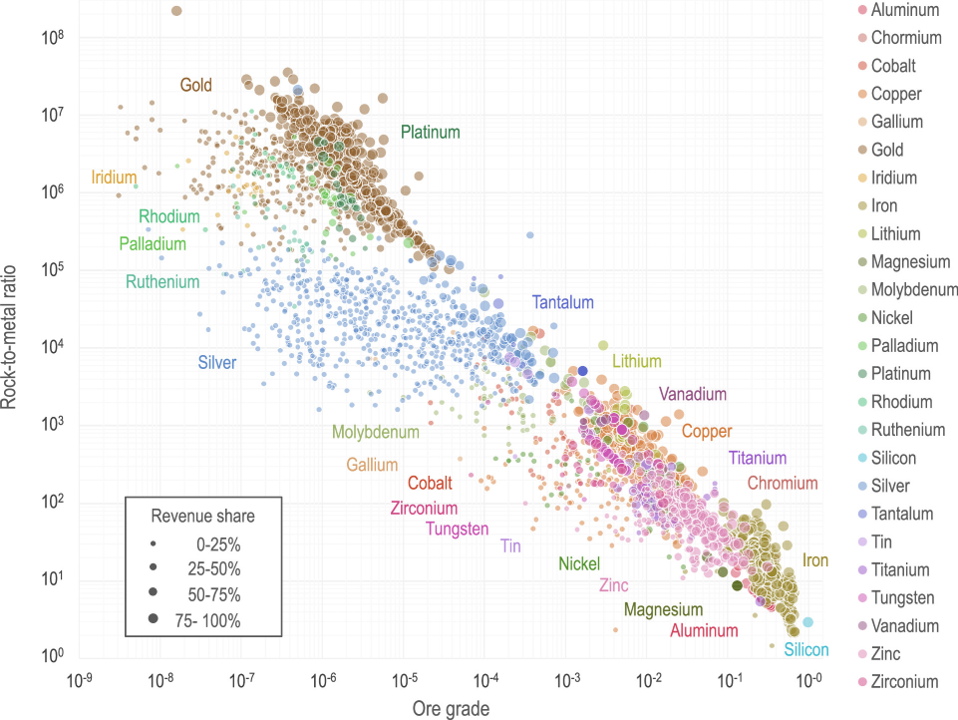

Scatter plots of Rock-to-Metal Ratios (RMRs) vs enrichment factor relative to continental crust (Clarkes), ore grade (economic concentration) in log scale.

The horizonal axis represents the work nature has done to concentrate an element, whereas the vertical axis represents the concentration required by society to recover an element.

Large circles represent global RMR averages; small circles represent individual operations

Nassar et al, Environ Sci Technol. 2022 May 17; 56(10): 6710–6721.

WA Array, valuable insight

Exploring where metals are

Integration of isotopic and seismic data

New insights from geochemical and isotopic mapping, seismic surveys, to reference this back to poorly mapped undercover geology, to increase our applied understanding of cratons, the evolution of their margins, and the associated deposits their bear.

Integration of DMIRS & GSWA work should help reveal the internal architecture, through various techniques covering data of varying amplitude, from crustal scale seismic reflection surveys, to passive seismic arrays, to regional isotopic maps, or whole rock geochemistry from publicly funded EIS drillholes.

Mine waste, tailings, landforms

Scaring the Earth

Preventing injury to the land is paramount, and a constant focus of the Akarbo environmental and project team. Rigorous assessments and approval process happen to ensure mine wastes and tailings are properly investigated through quantitative mineralogy and metallurgy, so that unrecovered critical minerals aren’t left unvalorised.

Ensuring the mines of the future are discovered

Making the world a better place ?

Akarbo's role in a "green" future

Mapping through cover

Translithospheric fault

The decarbonised mine

While the numbers are large, one should also keep in mind that the extraction of the 8.8 billion tons of coal we use is extremely material and water-intensive

Mobilising power in remote areas

We are looking for continuous and uninterrupted power supply for safety systems, communications, mission-critical assets and infrastructure across all operations. Our technology agnosticism stops where spinning reserve requires fossil-fuel support. The risk of power outage needs to be balanced with firmed capacity capable of handling fluctuations. We are keen on exploring high penetration wind and solar PV array associated with stand alone power systems and integrated battery storage, considering decommissioning liabilities, minimal land sterilisation footprint.

Electrified haulage ?

Is haulage required in the first place, or can the mine exclude altogether the requirement to get the mass of the truck on the move, when only the payload matters ? We are exited to investigated opportunities for in-pit / underground conveying systems, minimising the reliance of a transport fleet.

Fast tracking change

But how fast do we need to move ? In 2024, we are left with 200 Gigatonnes of CO2, which at an exhaustion rate of 40 Gt per year means a 50% likelihood to stay under 1.5 degrees would be exhausted by 2029. (alternatively, 67% chance exhausted in 2027, 83% chance exhausted by 2026). Source :

Letting the drillbit do the talking

With limited capital comes great responsibility. To optimise the allocation of finite resources, we have decided to limit our communication and representation expenses to the bear minimum. Walking the walk rather than talking the talk in essence.

Our carbon philosophy

Less is more. The fewer the better. Front, end and center. KPI it so that it’s part of all decisions. A productive day is producing no more carbon dioxide than we are through breathing.

(and a lil bit of methane because… we’ll are humans, rights ?! Or are we ? We co-host 100 trillion biota in our organism after all ! )

Influence over design

Limited shareholding means less possibles sources of conflict over decision making, as we care for a better future to make a difference. We need to start baselining our ideal emission profile aligned with the Paris agreement across all our emissions (Scope 1+2+3)

Decarbonisation fund

Should there be any gold recovered as a by-product of a commodity that matter (Cu, Bi, U,W,Fe, REE, P…), we vow to allocate all proceeds into a decarbonisation fund to invest in loss-making or difficult-to-finance initiatives that help us on our journey to mine responsibly. As a result of this core value, mining for solely for gold won’t happen as it won’t be considered a profit but a cost.

ASRS

We’re all for a mandatory climate-related financial disclosure and fully support the federal initiative for an Australian Sustainability Reporting Standard. We aim for best practise from the start and may have to undergo a readiness assessment in light of our future operational emission decarbonisation roadmap.

Ready to motor

Electrify everything, and minimise the transportation of things that don’t need to move. That’s how we make the best use of motors.

Sufficient level of capacity building

As a company, we are greater than the sum of our individual employees. To get where we ant to be, upskilling is essential and provisioning for it is too. That means being staffed at the right level to keep a good dynamic working environment, with a right balance for thriving personal life.

Doing the right thing from get go

Think first so you don’t act twice.

Building resilience

Plan ahead for some wild future.

Eagerness to go down the rabbit hole

Devil’s in the details. Let’s not be afraid to deep dive in the details to unravel the technical intricacies. Things are complex and oversimplification can hurt.

Leading the way

Let’s show how things should be done

Setting the example

Let’s show how things should be done

Our materiality approach

Everything matters. Not just CO2 ! We embrace the donut economics and see further than what the carbon tunnel vision has to offer. Keep biodiversity, disruption to N and P cycles, water, light pollution, aerosols, depletion of natural biotic and abiotic capital in the discussion and every decision making !

A "responsible" emitter, really ?

Safeguard legislation mandate polluters above 100 kt CO2e Scope1 to a set of light constrains. We think the scope of companies should be widened and the threshold halved, and be inclusive of the Scope 2 emissions.

Pricing negative externalities

Akarbo is in support of a generalised model of carbon price. For this price to have a meaningful effect on decision-making, we decide to voluntarily align with the social cost of carbon of US$1056 to reflect the present value of welfare loss associated with business as usual, as indicated in Bilal & Känzig 2024. We also price NOx emissions at AU$12800 (AU$3700-46700/t from Buonocore et al., 2014), Diesel particulate matter PM2.5 at AU$190000 ($AU$40000-410000/t) underground and AU$50000(AUD4-190000) aboveground (NSW EPA, 2013), Statistical value of life (for fatal injury) $5.4M (OIA, 2023)

Pushing the Earth System boundaries :

Exhausting the biosphere

Subverting the hydrosphere

Emptying the pedosphere

Rocking the lithosphere

The anthropogenisation of Nature is really what we have become excelling at

Nature is facing a serious human crisis

Akarbo is in support of a generalised model of carbon price. For this price to have a meaningful effect on decision-making, we decide to voluntarily align with the social cost of carbon of US$1056 to reflect the present value of welfare loss associated with business as usual, as indicated in Bilal & Känzig 2024. We also price NOx emissions at AU$12800 (AU$3700-46700/t from Buonocore et al., 2014), Diesel particulate matter PM2.5 at AU$190000 ($AU$40000-410000/t) underground and AU$50000(AUD4-190000) aboveground (NSW EPA, 2013), Statistical value of life (for fatal injury) $5.4M (OIA, 2023)